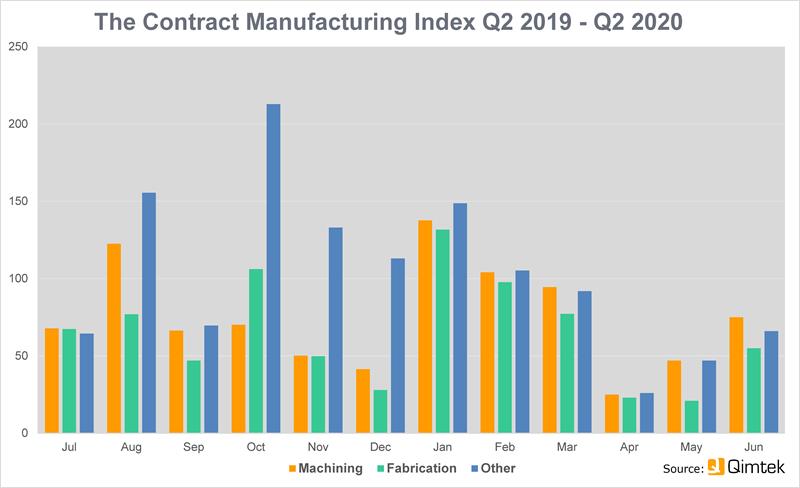

The CMI for Q2 2020 stood at 49, compared to 112 in Q1 2020. The baseline figure of 100 represents the average value of the subcontract manufacturing market between 2014 and 2018.

The Index shows a fall of 51% from the equivalent period in 2019.

Both machining and fabrication took a heavy hit – down 68% and 60% respectively on the previous quarter. Other processes, which include plastic moulding and electronic assembly, saw a much more modest fall of just 3% and accounted for 26% of the total market.

The market that suffered the most was Oil/Chemical/Energy – down by 90%, with Automotive, Food & Beverage, Construction and Heavy Vehicles/Construction Equipment also dropping sharply.

From a low base, Agriculture saw a big rise, while Furniture, Medical and Pump & Valve showed healthy growth.

The CMI is produced by sourcing specialist Qimtek and reflects the total purchasing budget for outsourced manufacturing of companies looking to place business in any given month. This represents a sample of over 4,000 companies who could be placing business that together have a purchasing budget of more than £3.4bn and a supplier base of over 7,000 companies with a verified turnover in excess of £25bn.

Commenting on the figures, Qimtek owner Karl Wigart said: “While business was obviously down during the months of April and May, when both machining and fabrication were hit hard, things started to pick up in June.

“We anticipate a continuing improvement in the third quarter as buyers have told us that they are looking at new projects, carrying out complete reviews of their preferred suppliers, and reshoring manufacturing.

“All in all, the outlook appears to be positive for those UK subcontractors that are in a position to take advantage of this.”